From the Frontlines of the Belt and Road

I was at the opening ceremony for China’s Belt and Road Initiative (BRI) in Solomon Islands in late 2022. In the shadow of the Gold Ridge mine overlooking Guadalcanal, Chinese lanterns and red banners in dual Chinese and English flew proudly above the audience as the Prime Minister of Solomon Islands spoke about the bright future of Sino-Solomon relations with the newly appointed Chinese ambassador by his side.

In the audience, mixed amongst officials from China’s state-owned enterprises, were many of the local leaders I was proud to work with on the original Australian investor-led iteration of the project in 2017. What should have been an opportunity for private investment to align with Western geopolitical interest had instead become one of China’s leading BRI projects in the South Pacific, with Solomon Islands well on track to becoming a client state. What went wrong?

Gold Ridge is the Main Asset in the Region

While remote and often forgotten, Solomon Islands sits at an active geopolitical crossroads with Chinese and Australia-led western interests competing for influence in the small but strategically located island chain. This is primarily due to its location on the sea lanes between the US and Australia and its central position amongst major islands of the South Pacific.

Since opening in 1998, the Gold Ridge mine (‘Gold Ridge’) has been the main economic asset in Solomon Islands, at peak producing 30% of national GDP. However, by the time I arrived in 2017, the mine was abandoned. Its most recent owner, an Australian company, left in 2014 after ongoing tensions with locals culminated in torrential rain which caused the mine’s tailings dam to fill to dangerous levels and foreign staff to leave the country. See Appendix A for more context on Gold Ridge and Solomon Islands.

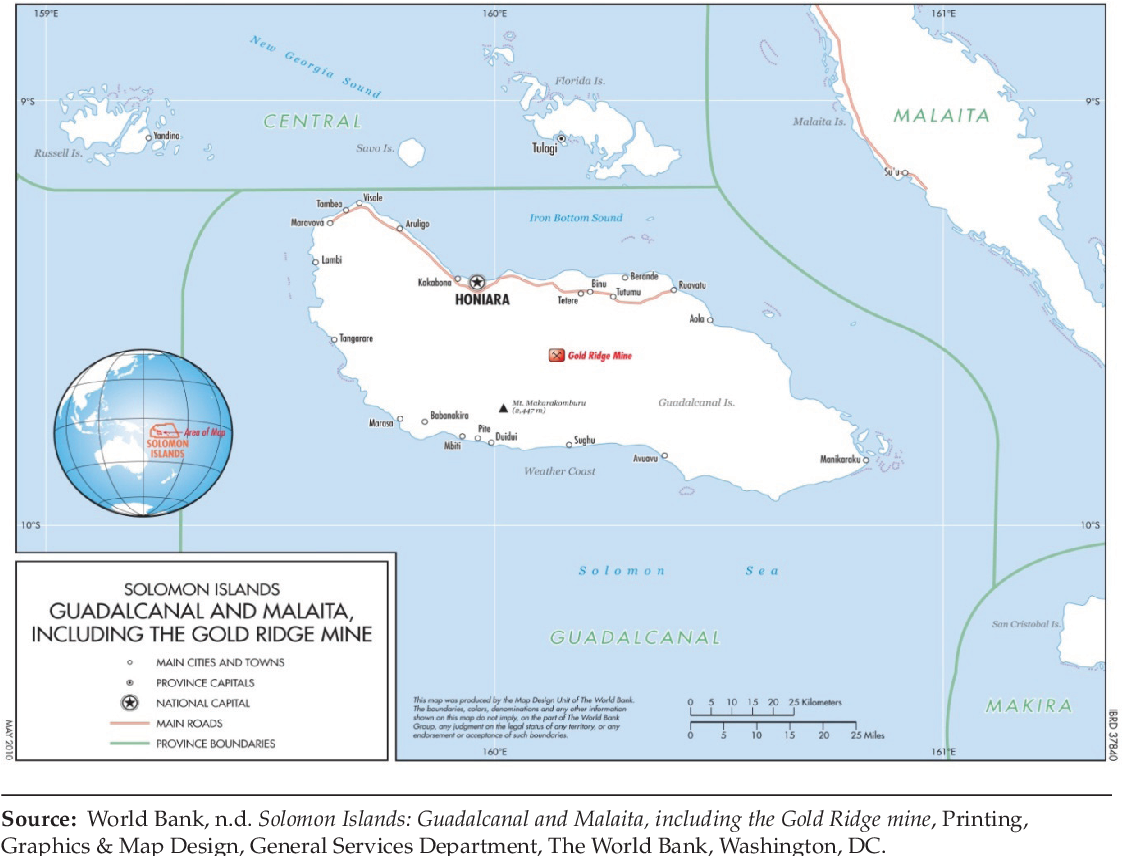

Figure 1. Map of Guadalcanal and Malaita, including Gold Ridge. Source: World Bank

Given this history, most people believed I was crazy for getting involved. However, a valuable gold reserve remained, and my firm believed that by partnering with indigenous landowners as joint-owners and operators, we could address many of the governance-related issues which had caused past foreign owners to come into conflict with local stakeholders.

Our goal was to rebuild the mine. To be successful, we needed to build support for a large project impacting diverse and conflicted groups in a challenging operating environment. This was aligned with national interest, and we had weekly meetings with cabinet; constant engagement with local landowners and cultural and religious leaders; as well as the milieu of diplomats, international agencies, and NGOs active in the region. Through that experience, we had a front-row seat to the BRI as it entered Solomon Islands, took over Gold Ridge, and expanded all over the country.

There is No Functioning Mining Investment Ecosystem in the West

The ultimate reason why Gold Ridge is controlled by China today is because we, as Australian mining investors and operators, could not secure the financing to develop it. True to our investment strategy, we were able to clean up the site, build community support, and win approval to reopen for a miniscule fraction of the multi-hundred million dollar liability which many estimated at the time; but a year later, in 2018, when it came time to make the $50 million investment required to rebuild the mine plant itself, we could not raise the money in the West.

The mine today makes well over $50 million in profit each year for its Chinese owners - how were no Western investors interested in such an asymmetric opportunity? Capital markets in the mining industry are uniquely dysfunctional. Imagine if Exxon, Shell, and BP pulled out of oil and gas exploration and development to become energy portfolio managers. That is analogous to what has happened in mining.

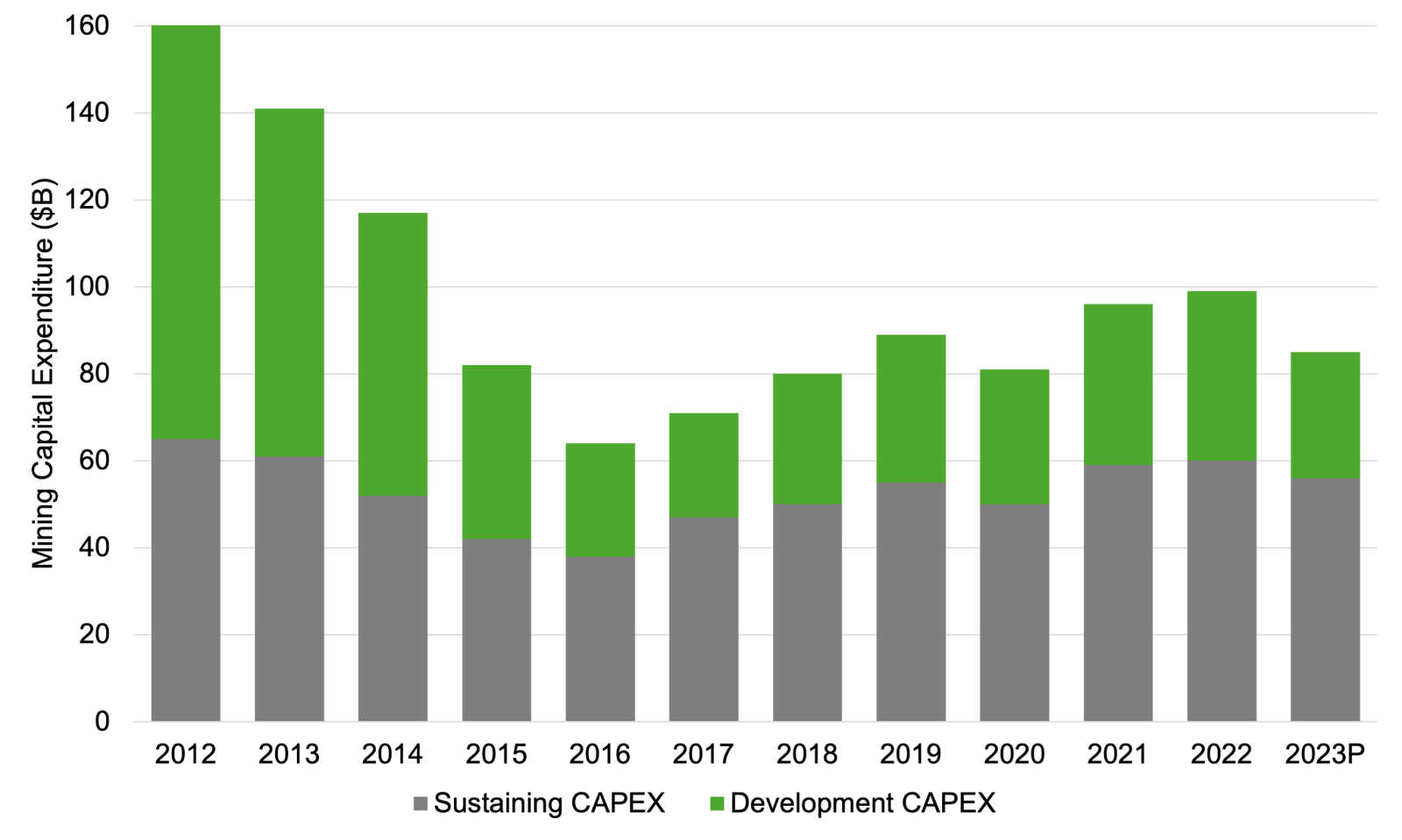

Like many industries, big companies in mining have gotten bigger. Over the last twenty years, the top 40 companies (‘majors’) have tripled in size to represent over half the capital in the industry. While not a problem in itself, as they have grown, they have increasingly departed from the smaller initial investments needed to find and develop mines to instead focus on growth via mergers and acquisitions. This has disconnected mine revenues and expertise from earlier-stage investment requirements. Due to this and other exacerbating factors, capital expenditure has dropped from $164 billion to $87 billion since 2012, with most of this focused on existing assets (Figure 2). Investment in exploration (a catch-all term for all pre-construction activities) has also fallen dramatically, from $20 billion to $12 billion since 2012. Finance and investing enthusiasts see Appendix B for more context.

Figure 2: Capital expenditure by major mining companies ($B). Source: S&P. Image description: Gray stacked bar chart. X-axis shows years from 2012-2023 and y-axis shows capital expenditure between 0-160$. Each bar consists of two categories: sustaining and development, and shows changing capital expenditure (mainly a decline) from 2012 to present.

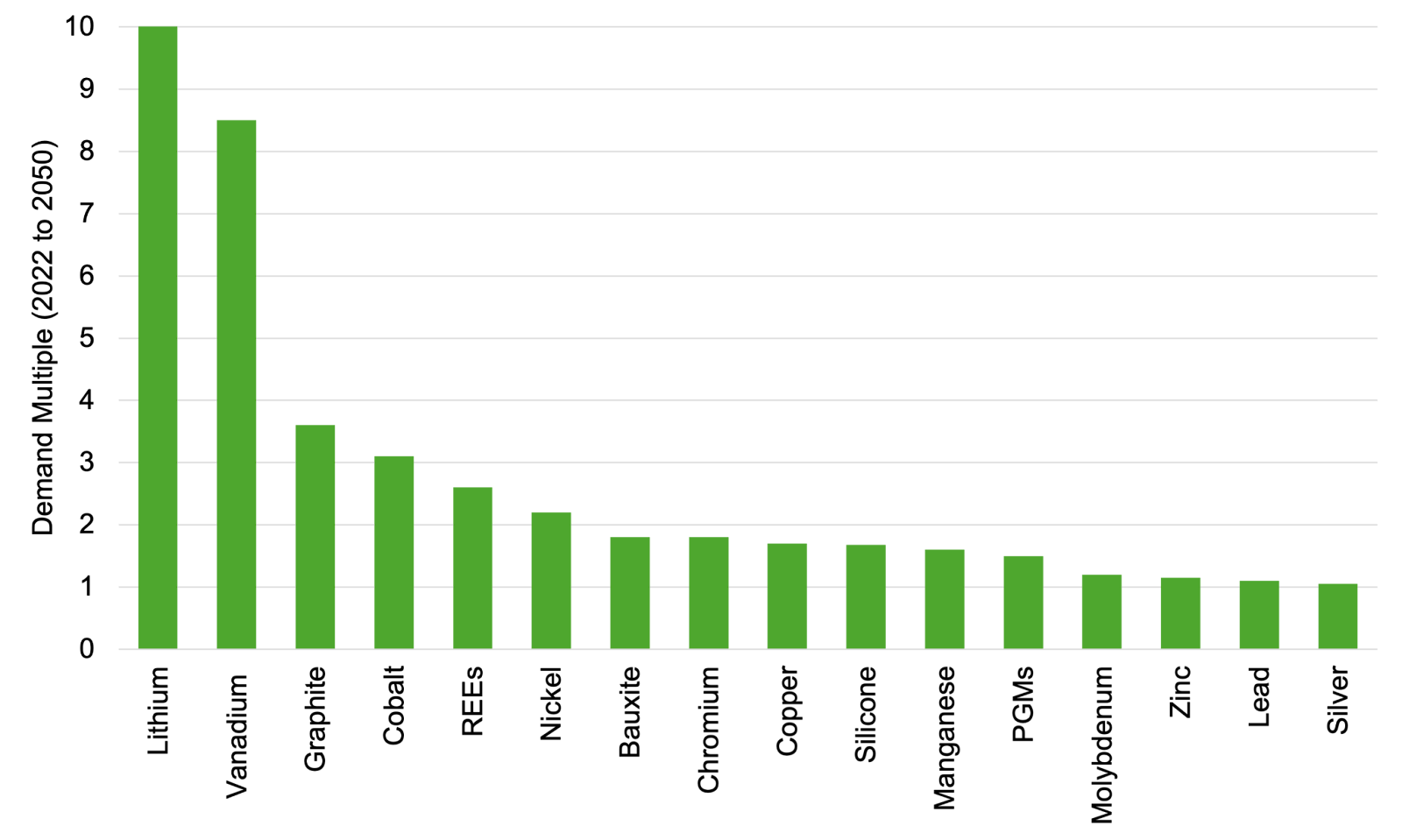

Unfortunately, this decline has coincided with the need for rapid supply growth for a list of critical minerals vital to the energy transition and other advanced industrial, consumer, and defense applications. This is a market failure. It threatens the energy transition and has led to shortages and a reliance on China-controlled supply chains, which has impacted everything from EVs to fighter jets. With the average lead time between the discovery and production of a new mine now 18 years, inadequate investment today may already pose an existential threat (Figure 3).

Figure 3: Ratio of 2050 to 2022 demand for selected minerals in a net zero scenario. PGM = platinum group metals, REEs = rare earth elements. Source: IMF. Image description: Gray bar chart. X-axis: critical minerals, and Y-axis: demand. The graph shows the International Energy Agency’s projected mineral demand as a multiple of 2050 to 2022 demand across 16 critical minerals. Notably, it shows that demand is expected to rise by a factor of 10.2 for lithium, 8.4 for vanadium, and 3.9 for graphite.

With the formerly diversified, integrated exploration and mining ‘majors’ now playing less of a role in exploration and in the early stages of new mine development, the industry has instead turned to public markets. The development of new mineral deposits (or mining ‘projects’) occurs in an apocalyptic scenario where thousands of single-asset, pre-revenue listed microcaps (‘juniors’ or ‘explorers’) of varying intent and quality compete for the attention of retail investors who have little of the capital depth or expertise needed to identify and back good assets past early exploration. With few professional investors involved, many juniors that are little more than ‘lifestyle’ focused have been able to proliferate, while for the majority, limited piecemeal funding means that a significant proportion of any capital raised has to be allocated to holding costs as opposed to efficient value creation. This has given the entire junior sector a poor reputation, perpetuating the cycle of underinvestment and stagnation, with only a few able to distinguish genuine opportunities amongst the thousands of struggling companies.

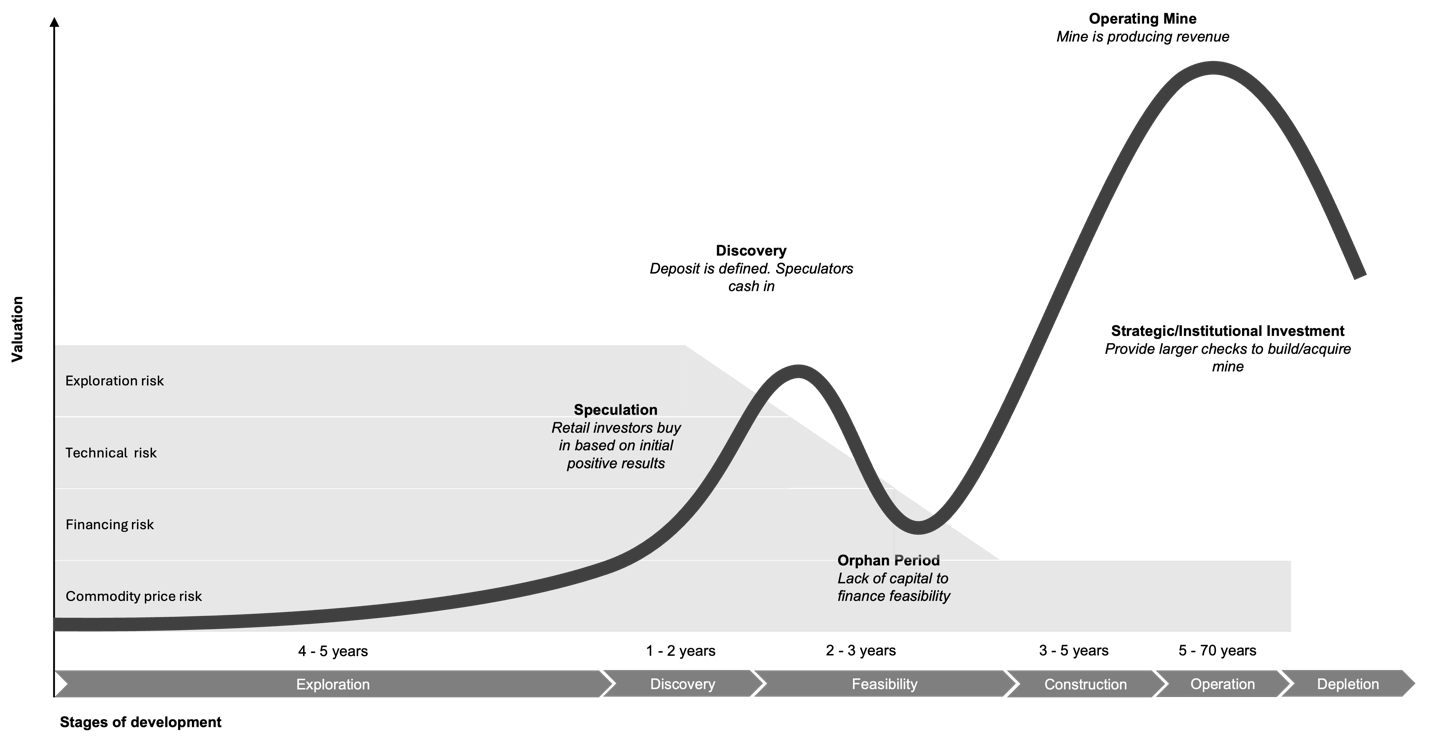

As a result, it is commonplace for even the best, most strategically important mining assets to languish for years between exploration and development, often passing through the hands of multiple owners waiting for the necessary finance and expertise to come into place to progress. This financing gap is sometimes referred to as the ‘orphan period’, with it actually possible to invest in proven mineral deposits at a lower valuation than exploration (Figure 4).

Figure 4: Lassonde curve representing the life cycle of a mining company with x-axis featuring the stages of development and y-axis, the valuation. This was exactly my experience at Richmond Vanadium, where we acquired the world’s largest vanadium deposit and achieved a 6x return by driving it past pre-feasibility (Appendix C). Source: Pierre Lassonde. Image description: Gray Lassonde curve. X-axis: Stages of development; and Y-axis: Valuation. The curve shows the typical changes in valuation as a mine progresses through development stages: exploration, discovery, feasibility, construction, operations, closure. The chart background shows risks associated with each stage. Notably, it shows that mine valuation falls after discovery stage despite reduced risk due to a lack of investment focused on feasibility stage.

In contrast, Chinese companies can invest with confidence that they will be able to find the partners they need to hold, sell, or develop their mining projects as appropriate, allowing assets to be efficiently developed. They are frequently vertically integrated all the way from mine to manufacturing, bringing together revenue streams and expertise. China’s recent dominance in nickel, which has forced many Western producers to close, is in no small part due to the development of less than ESG-friendly mines in Indonesia by Chinese battery makers. This and other examples stand in stark contrast to the fragmented exploration, mining, and manufacturing industries as well as their respective capital markets present in Western economies.

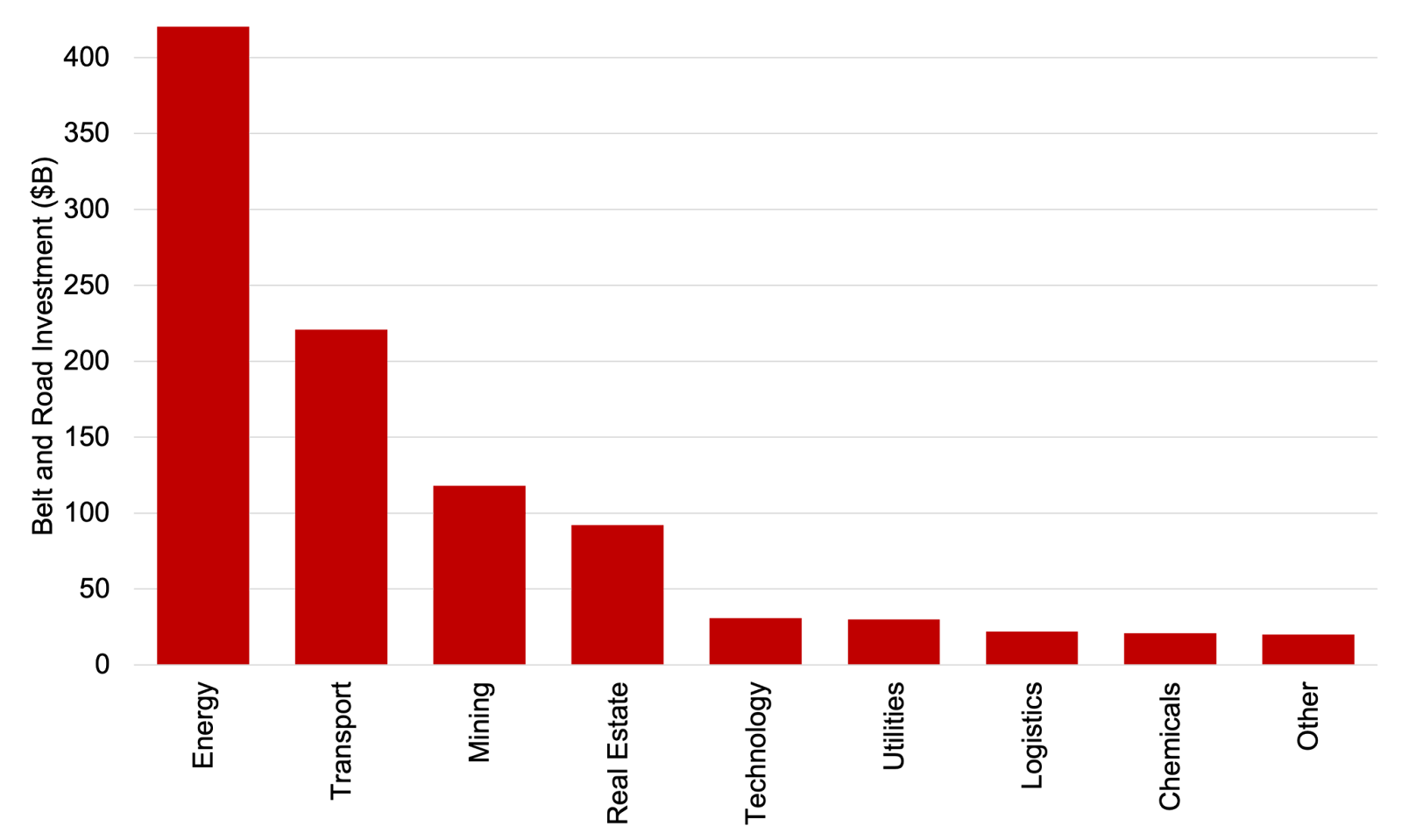

This desire to invest is fed by the Chinese government through the BRI and its forerunner, the Going Global Strategy, which together have allowed Chinese companies to pursue opportunities with the benefit of government alignment and support (Figure 5).

Figure 5: Cumulative BRI engagement by industry between 2013 and 2023 ($B). While mining is less discussed in the context of the BRI, it forms a major part of China’s strategy. Source: Green Finance and Development Center. Image description: Gray bar chart. X-axis: industrial sector; and Y-axis: Belt and Road Initiative investment in billions of US dollars. The graph shows that while mining is less often discussed in the context of competition with China, it attracts the third highest level of Chinese government investment, totalling $118B to date, ahead of real estate and technology.

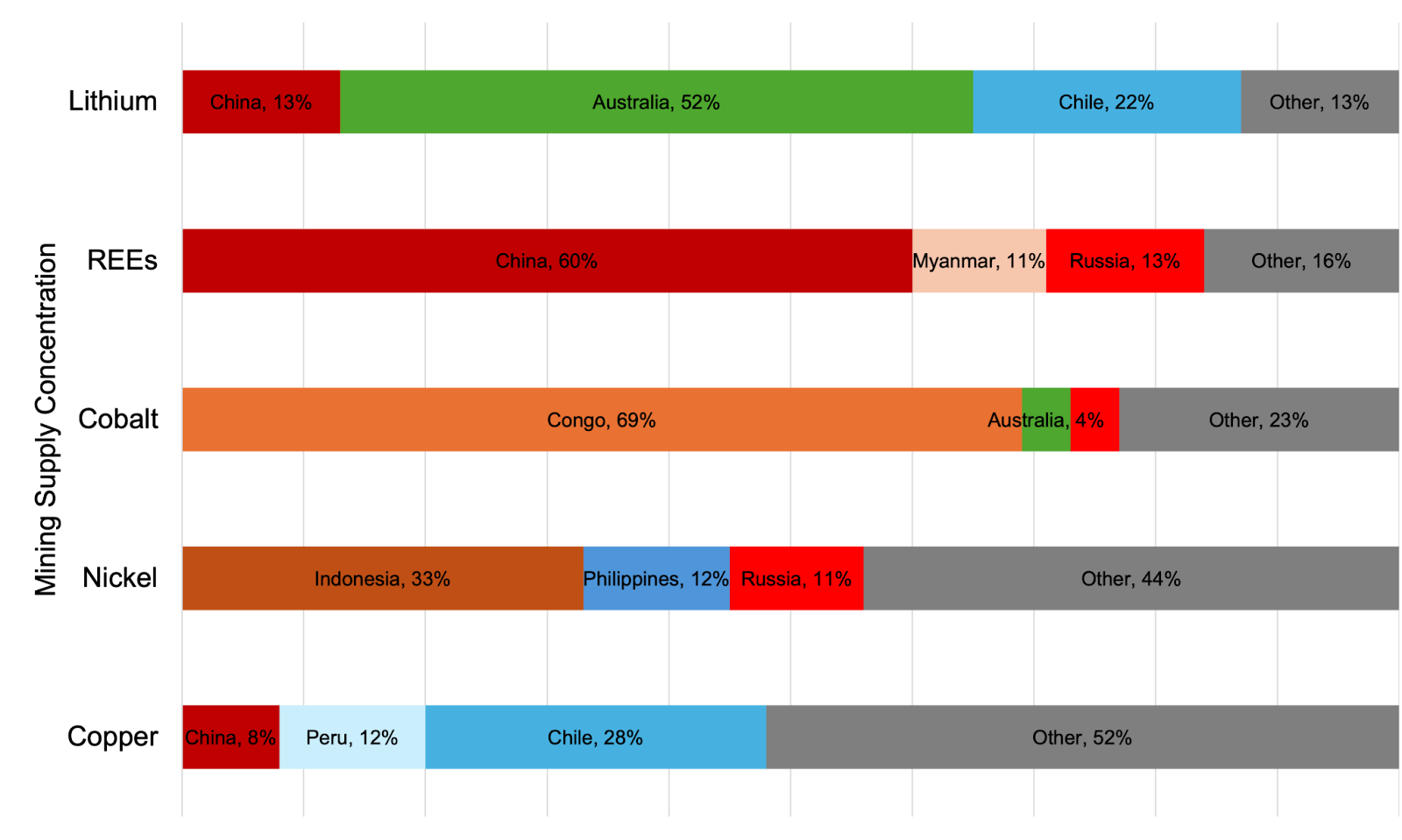

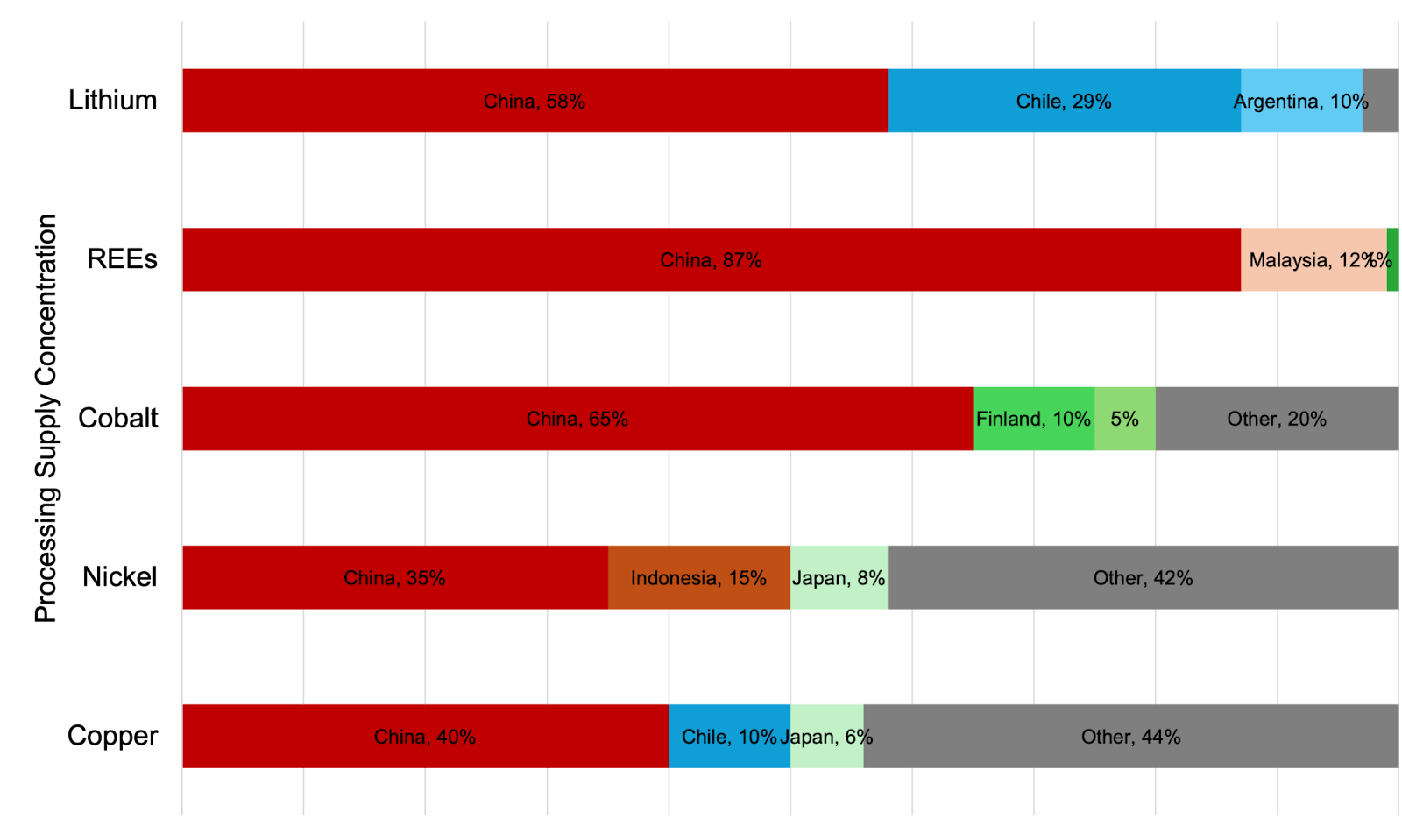

Investment in mining through the BRI is at an all-time high, reaching $19 billion in 2023, and expected to continue dramatic growth. Chinese investment has also been forward-looking and focused on minerals needed for energy and defense. In contrast, Western financiers have remained focused on traditional commodities, with more invested in gold than all other commodities put together, and iron, copper, and coal making up most of the balance. As a result, China dominates the mining supply chain for clean energy, including over 50% of the world’s lithium, rare earths, nickel, cobalt, and graphite; as well as their associated geographies through mines like Gold Ridge (Figure 6).

Figure 6: Mining supply chain by geography categorized by mining and processing. China owns almost all the cobalt mines in Congo, nickel mines in Indonesia, and major stakes in lithium mines in Australia. Source: IEA. Image description: Two horizontal stacked bar charts titled Mining and Processing. For each chart the Y-axis features 6 critical minerals: lithium, REEs, cobalt, nickel, and copper, and the X-axis is a stacked bar showing the percentage of geographical concentration for the mining and processing of each mineral by country. The graphs show that China accounts for 60% of rare earths mining, and over 50% of lithium, rare earths, and cobalt processing.

For more context on mining and the energy transition, see Appendix D.

The Belt and Road is Not a Centralized Monolith

By mid-2018, the lack of Western financing options for Gold Ridge forced us to seek an equity partner. This wound up being a mid-cap Hong Kong-listed mining company. Far from a Chinese state-owned enterprise swooping in with an overwhelming offer, or simply collaborating with government to take over as has happened to other Australian companies in Africa, it started as a typical private sector deal wherein the Hong Kong company would buy out just over half of Gold Ridge and fund reconstruction.

However, by mid-2019, the deal was stalled. Articles began to appear on how their push, and therefore China, may fail in Solomon Islands. This inaccurate conflation of the Hong Kong company with the Chinese government is paradoxically what likely prompted the first serious attention from the Chinese government. After over a year of struggling, by late 2019 one of China’s largest state-owned enterprises agreed to become both their lender and lead contractor to complete the acquisition and rebuild the mine. Far from entering Solomon Islands at the direction of some central planning authority, it was instead middle level executives who stepped up after being introduced to Gold Ridge by China’s relatively junior diplomats in the region (see Appendix E for more information on the deal).

Private Sector Led the Way to Diplomatic Recognition

The Solomon Islands officially recognized China over Taiwan in September 2019, shortly before the announcement of the state-owned enterprise’s involvement in Gold Ridge but well after the first Chinese personnel arrived on the ground. It is worth emphasizing the degree to which the private sector led the government over diplomatic recognition. The country’s national security advisor-equivalent confided that the influx of Chinese traders that would follow Gold Ridge was more than the government could hope to control. While there had been feelers between the two countries in the past, new urgency was brought on by the need to regulate the activities of these ‘frontier-style’ entrepreneurs. The national government saw the presence of the Chinese government on the ground as one of the only ways to achieve this.

Despite the upside of partnering with the far better resourced Chinese government, this was still no easy decision, as decades of funding and engagement from Taiwan had earned the loyalty of many in the country. Recognition of China over Taiwan caused riots in the capital and even an attempt to depose the government in 2021.

Competing with China is Far From Hopeless, We Just Need to do the Bare Minimum

While China is in the lead for critical minerals, as well as in broader influence in many nations in the developing world; the reality I saw in Solomon Islands was far from hopeless for Western interests. It was not destiny.

The Belt and Road Initiative is not unbeatable. What I saw was a loosely affiliated group of public and private interests of all levels of competence, resources, and drive. They may have won over Gold Ridge and then Solomon Islands, but this happened in a far from organized way. The Hong Kong company struggled through their original smaller intended investment, and at one point were in default. Their staff and those of the larger state-owned enterprise frequently alienated and caused conflict with locals, leading to protests. Despite this, they had patient and ultimately gratuitous capital - which can rescue any operator from disaster. They were able to hold on to Gold Ridge through a last-minute firehose of funding from China to build more infrastructure than the country had ever seen, and even this caused riots, which very nearly changed the government. They won in an absence of competition. Reflecting on our efforts, even a modicum of alternative finance would have allowed us to hold Gold Ridge without the need for Chinese investment, while less than a tenth of the development finance later available to Chinese interests would have allowed us to rebuild the mine as the model of landowner-driven sustainable development it was originally intended to be.

In order for the United States and its allies to compete with China, not only in mining but in all strategic sectors, we need to ensure that there is a funding pipeline which can bring good projects through development, backed by a minimally viable fraction of the capital available to Chinese interests. This capital, if deployed by investors and operators who are able to take an intelligent view on risks and invest the right amounts of capital at the same stages as Chinese competitors, could secure positive outcomes for all Western stakeholders, whether it be governments seeking to compete in strategic industries and geographies, manufacturers seeking to clean up and secure their supply chains, or investors simply seeking what can be large multiples underpinned by the value of a real asset. This would allow the US and its allies to beat China for geographically strategic assets like Gold Ridge and Solomon Islands, and the critical minerals assets relevant to energy and defense that we need to protect our countries, industries, and future.

After all, for all of China’s later financial advantages, we were still smart enough to be there first.

The views expressed in this article are those of the author and do not represent those of any previous or current employers, the editorial body of SIPR, the Freeman Spogili Institute, or Stanford University.

Stanford International Policy Review

Want to know more? Click on the following links to direct back to the homepage for more amazing content, or, to the submissions page where you can find more information about being a future author!